.png?width=2167&height=417&name=Greenrock-Logo%20(1).png "Greenrock-Logo")

Share this

by Bob Southard on Oct 24, 2023

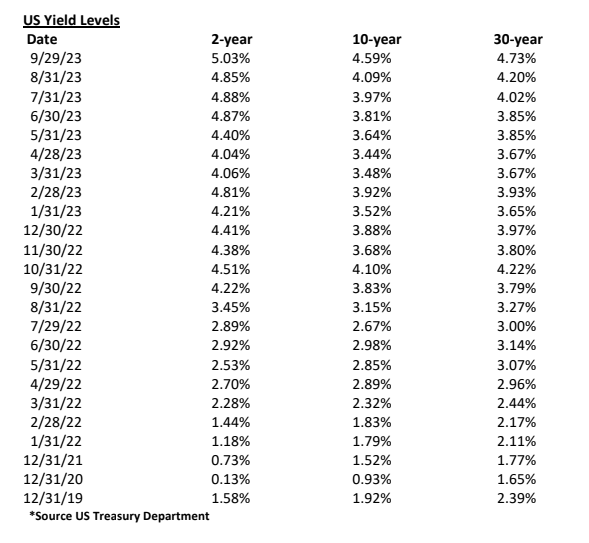

Short maturity interest rate levels rose but significantly less than the rates for intermediate and long-term rate levels with the Fed not having hiked rates since July.

Bloomberg Barclay's Fixed Income Index Returns

The Mortgage Market Asset Class had continuing problems with rising Mortgage Rates.

September Economic News

On September 1st the Department of Labor reported 187,000 jobs were added though the unemployment rate rose from 3.5% to 3.8%, its highest level since February 2022. The combined June and July employment reports were revised down by a total for the two months of 110,000 jobs. The DOL reported 22 million jobs had been lost during the pandemic years but an average of 400,000 new jobs have been added each month since. The DOL report indicated average hourly wages had risen by 8 cents for the month to $33.82, though the yearly increase is 4.3% down from 4.4% last month. The report indicated the labor force during the month even with 34,000 having lost their jobs with the shutdown of Yellow Trucking. Available job openings number is the lowest since March 2021.

On September 11th CNN reported US household wealth hit a record $154.3 trillion at the end of the 1st Quarter. Also, on September 11th Goldman Sachs cut its projected risk of a recession from 35% to 15% over the upcoming 12-month period.

On September 20th the debt of the US Government was reported to have increased to $33 trillion. This number became a focus point with the shutdown looming. Though the shutdown is temporarily stalled, if it had happened all nonemergency government employees would have been laid off, totaling 800,000 workers at average salaries of $95,000. This same shutdown may exist again in less than three months from now.

Also, on September 20th the Fed meeting reported rates were being held steady. However, Chairman Greenspan testified we should expect at least one future rise to fight inflation. On September 27th the US Emergency oil reserve was reported down by 270 million gallons this year. That represents its lowest level since August 1983. The US Government has indicated it would begin buying more oil toward rebuilding this level, except it feels it is too expensive to do so at this time! Is there really a feeling in the US Government that the price of oil will be declining in the near future, or instead, there is no need to rebuild the level of the reserve? Neither position makes any sense to me.

The US Commerce Department, one of the Agencies several of the Republican candidates want to do away with, reported personal spending rose 0.4% in August following the 0.9% rise in July. Personal incomes were up 0.4% in July and the savings rates were at 3.9% in August compared with 4.1% in July.

On September 28th CNN reported mortgage rates were at 7.31%. This is the highest level in 23 years. A week ago, the rate had been 7.19% and a year ago it was 6.7%.

With this rise in mortgage rates and the concerns about inflation being hyped by early political posturing (though more on that later), and the clear strength of the economy being misrepresented again for political gains, the US Commerce Board reported consumer confidence fell to its lowest level in four months.

This is an early sign of the concern I have been raising about the negative impacts the 2024-year election is going to have on the economy and country. On September 25th Mercer reported on a survey of 900 major clients spread across 15 industries. The survey result was that merit increases are expected to be 3.5% in 2024, down from 3.8% in 2023. Separately total salary increases are expected to be 3.9% in 2024 compared to 4.1% in 2023 and promotions expected to total 8.7% compared to 10.3% in 2023. All results from the survey were what I would characterize as pessimistic at the employer level, with the consumer level not being especially optimistic.

My Economic Outlook

I am going to open by repeating a concern I have been raising for months. It is time for Congress to stop playing games with impeachments and take up the long-term funding requirements for Social Security and Medicare. I continue to suggest these issues need to be addressed before we fully enter the 2024 election cycle. Without concrete solutions, the two programs will soon be approaching bankruptcy and likely become a political football between the two parties.

Now I am borrowing the September discussion from a very long-term friend, Clyde Kendzierski who authors each month "The 70% Solution" that I recommend everyone begin reading. In his September issue Clyde explains, "The rise in rates reduced the value of bank assets by over half a trillion dollars. Regulators permit banks to ignore those losses as long as they can maintain sufficient capital and deposits to fund the assets on their books." He continued, "Regulators bailed out the banks this spring but are now pushing banks to increase capital levels. Those requirements will dramatically reduce the lending capacity of affected banks."

His discussion moves to detail why consumer prices will rise in 2024 between 3% to 5% range. His expectation is inflation will hover around 4% and growth will decelerate toward a stagflation level. He then believes a recession will ensue and reduce inflation toward a 3% band.

I do not agree with this expectation but if he is correct, I agree with his outcome that conditions will be bullish for bonds from current levels.